Forecast 2024: It’s different this time...until it isn’t for commercial vehicles

26 September 2023

ACT Research: Commercial vehicle demand expected to falter but seeds of growth will be set

Ken Vieth, president and senior analyst for ACT Research

Ken Vieth, president and senior analyst for ACT Research

Ken Vieth is president and senior analyst for ACT Research, a publisher of commercial vehicle truck, trailer, and bus industry data, market analysis and forecasts for the North America and China markets.

Fueled by a pandemic-triggered shift in consumer spending and assisted by two years of government stimulus, freight volumes exploded in 2021. With the pandemic devastating globalized supply chains, the industry was unable to ramp up capacity in the face of unprecedented demand for commercial vehicles (CVs). That collision of irresistible force and immovable object created significant and sticky pent-up demand that powered strong production through a weak 2023 freight environment.

Weak freight markets and stronger if still top-side constrained build rates will effectively absorb lingering 2021 pent-up HD demand by the end of 2023. As we look to discern production levels in 2024, for the first time since before the pandemic, we believe new vehicle demand will be driven more by current trucking fundamentals than by special factors. Broadly speaking, those freight market fundamentals are not good, with most at “bottom of cycle” levels. Weak freight and soft profits mean medium-duty (MD) Classes 5-7 and heavy-duty (HD) Class 8 production volumes should fall in 2024.

It’s not different this time; yes, it is!

We start with a brief review of last year’s did-not-happen-after-all first half ’23 recession. Missing those foundational assumptions led our year-ago forecasts awry as Classes 5-8 vehicle demand did not soften in second half 2023.

With oil over $100/bbl, inflation north of 8%, real disposable income contracting and the yield curve inverted to levels not seen in 40 years, we expected the U.S. economy to tumble into a shallow recession. Instead, the economy in 2023 is beating expectations across multiple fronts — jobs, wages, oil prices, inflation, corporate cashflows, consumer savings/spending and the IRA economic stimulus program.

Not only did the economy not fall into a recession, but GDP growth the past four quarters has been 2.6%. Full-year 2023 growth is expected at 2.3%.

All graphs: ACT Research

All graphs: ACT Research

With real income growth rising, there are tailwinds heading into 2024. Our forecast is optimistic relative to the consensus at 2.2% GDP 2024. A year ago, ACT’s Freight Composite was projected to contract by -3.2% in 2023. The current forecast is for a more modest -0.5% contraction. While running flat y/y in Q3, the Composite anticipates 2.3% growth in 2024 before accelerating to 3.4% in 2025 as freight-heavy economic segments gain traction.

Rock and a hard place: Path to 2027

There is an expensive mandate in the long-term forecast that will drive a large prebuy. The EPA’s January 1, 2027 clean truck mandate lines up with what we anticipate will be the peak of the freight cycle into the end of 2025, and lagged carrier profits into 2026.

The last time we had a costly regulation (EPA’07) line up with the freight cycle (’04-’05) and carrier profitability (’05-’06), we estimated 100,000 Class 8 trucks and tractors were pulled ahead, and MD inventories grew by 40k units in the prebuy period. In Class 8 terms, the EPA’07 added new purchase cost was around 8%. With new technology and warranty extensions, we believe the cost of an EPA’27-compliant tractor will rise by around 12%, if less for fleets who already buy extended warranties.

Our question is: “Will EPA’27 costs cause some fleets to get a head start on fleet optimization in 2024?” We believe the industry will underscore to fleets that expected future costs and demand support are imperative to maintain supply chain viability and keep hard-won labor in place now to support soaring demand into 2026.

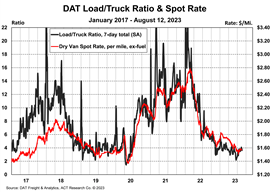

Not good right now for truckers

DAT’s load-to-truck series (SA) has risen from a cycle-low 2.2 loads-per-truck ratio in early June to 4.0 loads/truck in early August. As illustrated, the last two Class 8 demand upcycles were presaged by sharply higher ratios (Q2’17, Q3’20). LTL carrier Yellow’s failure coupled with improving economic fundamentals hint that underlying supply-demand conditions are on the cusp of improving.

Spot rates, a critical early directional indicator, remain stuck at low levels, and contract rates (not shown) need to fall by around 15% to achieve equilibrium with current spot levels. Our research suggests spot rates are currently running about 18% below operating costs for smaller trucking companies that have been falling out of the market at a rapid rate since last October. This is a good point to interject that carrier profitability and heavy vehicle demand are highly correlated.

The load-to-truck imbalance and corresponding weakness in freight rates underscores the publicly traded truckload carriers’ travails in Q2. During the quarter, this collection of 12 national carriers saw revenues fall 18% y/y, net income drop 44% and profit margins shed 270bps to 5.2% (-34%), a six-year low.

Heightened importance: 2024 order season

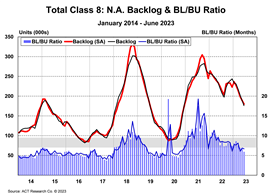

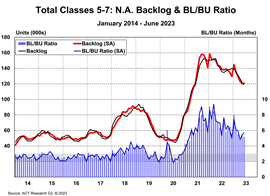

The June-ending NA Class 8 backlog stood at 175,200 units. Only 11,300 of those orders were scheduled to be built in 2024, with the remaining 163,900 set to be built in 2023. We do not have a similar Classes 5-7 analysis, but we would characterize the June-ending 118,800-unit MD backlog as almost entirely 2023-resident.

With the absence of the pent-up tractor demand cushion that supported 2023 production, the upcoming 2024 order season will stand on its own merits. While the economy is doing well broadly, with order season on the doorstep, it might not be doing well enough fast enough: Freight markets are expected to wallow in the current upside-down supply-demand environment into late Q1’24.

A weak freight market at the point when fleets are making capex decisions is not historically conducive to strong demand. Positively, capacity is leaving the market, and the economy appears to be increasingly supportive as consumers gain strength and inventory destocking concludes.

Unlike Class 8, unmet Classes 5-7 demand will linger into 2024. The residual overhang stems from OEMs deciding (where applicable) to direct more shared components to higher margin HD products at the expense of the MD production. Given the service-based nature of MD vehicles, pinpointing pent-up demand is challenging. Using a variety of current market metrics, including backlogs, build and orders, end of 2023 pent-up estimates between 30,000 and 40,000 units are defensible.

In line with weaker freight data, demand for MD vehicles has moderated over the course of 2023. Reflecting the change, June-ending backlogs were down 15% y/y, while inventories accumulated due to higher OEM throughput and still-constrained body builder networks. Inventories in June were up 32% y/y to 78,200 units.

Strong sales continue to absorb the industry’s higher Class 8 build rates. At the end of June, Class 8 inventories were unchanged since last October at 60,700 units. The absence of a major inventory overhang will lessen the drag typically experienced into a market downturn.

While there is strong visibility into year end, improving economic signals and continued weak freight metrics make for interesting bedfellows as 2024’s order season starts in earnest in 2023’s last trimester.

Forecasts

A substantively out-of-balance freight environment into the second half of 2023 all but ensures that MD and HD CV demand is heading lower in 2024, as margin compression tightens buyers’ capex. The HD market will also feel the absence of pent-up demand and the correction of overcapacity that will weigh on near-term demand.

Bright spots include healthy vocational markets, strong activity in Mexico and defensive fleet positioning ahead of the expensive EPA’27 mandate, all of which should help moderate the anticipated topline downturn in 2024. Ongoing pent-up demand and supportive U.S. consumer balance sheets make for a very shallow MD Classes 5-7 demand trough in 2024.

With better U.S. economic footing and the retail inventory correction fading, the seeds of stronger CV demand will be planted in 2024, sprouting a 2025 demand recovery.

STAY CONNECTED

Receive the information you need when you need it through our world-leading magazines, newsletters and daily briefings.

POWER SOURCING GUIDE

The trusted reference and buyer’s guide for 83 years

The original “desktop search engine,” guiding nearly 10,000 users in more than 90 countries it is the primary reference for specifications and details on all the components that go into engine systems.

Visit Now

CONNECT WITH THE TEAM