Gen-set supply chain gets back on track

27 November 2023

2023 brought fewer supply constraints and growth in total gen-set production

When we look back at the last year and consider how the North American production of gen-sets has fared, thoughts of a looming recession on the horizon for early 2023, as well as continued supply chain effects surrounding critical parts, dominated the conversation. Nearing the end of 2023, it’s interesting to review how both these key situations have progressed.

Diesel gen-sets for commercial and industrial applications will see a 3.2% increase in production from 2022 to 2023. (Photo: KHL Staff)

Diesel gen-sets for commercial and industrial applications will see a 3.2% increase in production from 2022 to 2023. (Photo: KHL Staff)

Looking at the recession topic, I know I had an uneasy feeling of “when is this recession going to rear its head” as we entered 2023. Before we knew it, we were into the second quarter and there were not the signs of recession that onewould traditionally associate with a pullback or downturn in the economy. We went to trade shows and visited industry participants and concerns of a slowdown due to recession were really on the backburner, if even mentioned at all. From all respects, the outlook within the power equipment industries in North America was quite positive, with more of a focus on forging ahead and working through existing supply chain constraints.

On the consumer end of things, a useful barometer for recession is to observe trends in the auto industry. Demand continues to remain strong for new automobiles; but one could argue that we have pent-up demand due to a couple of years of low inventory, thus supporting the shorter-term demand strength. Nonetheless, consumers do not seem to be wary of the economy overall, even with a series of interest rate hikes over the last two years to help curb inflation.

Inventory levels rebound

The supply chain issues affecting the production of gen-sets appear to have greatly eased compared to one year ago.

In the Power Systems Research PowerTracker syndicated survey, we speak with 200 gen-set dealers each quarter. Over the course of 2023, we have seen a significant downward shift in the percentage of dealers who cite a lack of inventory as a reason for not selling more gen-sets.

One year ago, a significant percentage of comments surrounded the notion that dealers were held captive to a supply constrained market and just could not get needed inventory. The order lead times were still too long, and they lost sales because of those lead times.

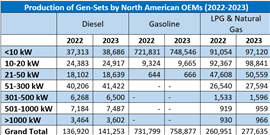

North American generator set production from 2022-23. (Table: Power Systems Research)

North American generator set production from 2022-23. (Table: Power Systems Research)

There were eight consecutive quarters of reported decreases in overall inventory from gen-set dealers from Q2 2020 through Q1 2022. Starting in Q2 2022, dealers slowly started building back inventory over the course of 2022 and through the first quarter of 2023. In the second quarter of 2023, dealers reported that inventory had slightly decreased by 1% while overall sales for the quarter had decreased by 4.6%.

With lower quarter-on-quarter inventories and lower quarter-on-quarter sales, this is a true signal that dealers have pulled back on new orders from the factory and are comfortable with current inventory levels once again. We do feel, though, that with the cyclicality of the gen-set production pattern that the third quarter and fourth quarter of 2023 will prove to be strong in sales, as weather patterns and continued strong home standby demand will push 2023 higher in terms of total gen-set production relative to the 2022 year.

Demand continues

The demand for residential use and home standby units has held up well. Many homeowners are opting for standby gen-sets – most often powered by natural gas or LPG fuel – due to more volatile weather events and issues related to an aging grid infrastructure leading to more frequent and longer power outages over the last few years.

Although the higher interest rates will push away some of those purchases, overall that portion of demand has remained strong for the home standby market. We see production for natural gas and LPG units at 6.4% higher from 2022 to 2023 when all is said and done.

Joe Zirnhelt, president and CEO at Power Systems Research

Joe Zirnhelt, president and CEO at Power Systems Research

Finally, commercial and industrial demand has maintained pace over the past year. The diesel gen-sets that are an important product area for these users will see an overall increase in production of 3.2% year-on-year from 2022 to 2023.

This increase recognizes a two-fold effect of supply and demand. First, dealers have been replenishing inventories up to planned levels. Second, on the demand side, dealers have observed overall a healthy level of investment by businesses for fixed standby units. At the same time, projects originating out of the bipartisan infrastructure bill enacted in August 2021 have really sustained many parts of the diesel industry for rental and construction companies carrying out these infrastructure projects.

Joe Zirnhelt is president and CEO at Power Systems Research, an information and research supplier based in St. Paul, Minn., with offices in Detroit, Brussels, Tokyo, Pune and Sao Paulo. He can be reached at [email protected].

STAY CONNECTED

Receive the information you need when you need it through our world-leading magazines, newsletters and daily briefings.

POWER SOURCING GUIDE

The trusted reference and buyer’s guide for 83 years

The original “desktop search engine,” guiding nearly 10,000 users in more than 90 countries it is the primary reference for specifications and details on all the components that go into engine systems.

Visit Now

CONNECT WITH THE TEAM